I recently did a post‑mortem on a project, and the more I look at it the more excited I get, #Unitas ( @UnitasLabs). 🧐

It's not because $UP went up. It's because I want to understand why, when the broad market is falling, it keeps rising?

Many might think it's "just another stablecoin issuer", but if you dig into its secondary‑market token $UP, which is making new highs against the trend with explosive volume, you'll see that its ambition is far beyond a stablecoin.

Its next big move is to become a yield‑asset layer on BNB Chain.

A stablecoin aims to "anchor a price", whereas a yield‑asset layer aims to "keep money working on‑chain continuously". The difficulty of these two goals is on completely different scales.

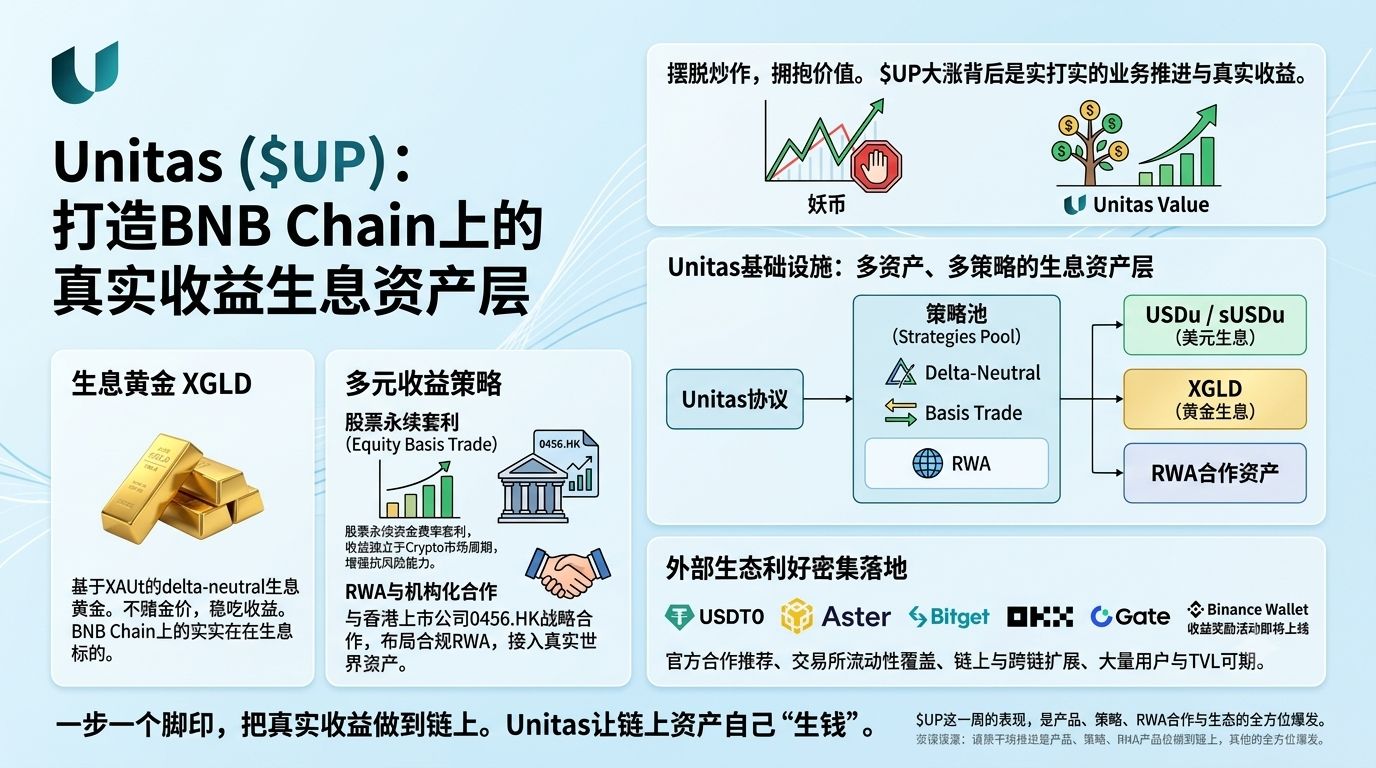

In simple terms, a yield‑asset layer turns on‑chain capital (USD, gold, US equities) into a constantly laying hen via a robust strategy that "doesn't bet on market direction, only on arbitrage".

Now, let's see how it works – three steps, each building on the previous, and each quite interesting:

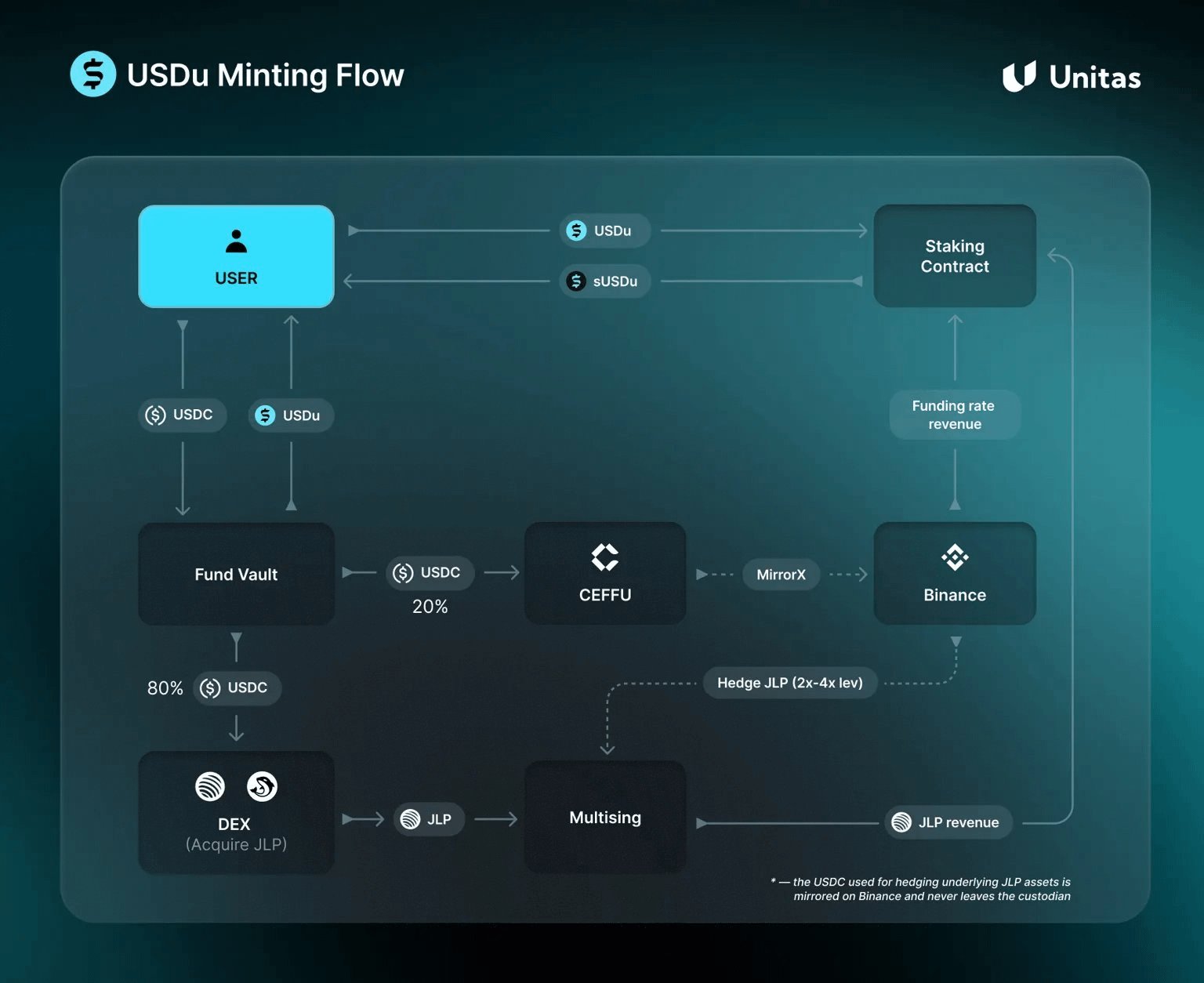

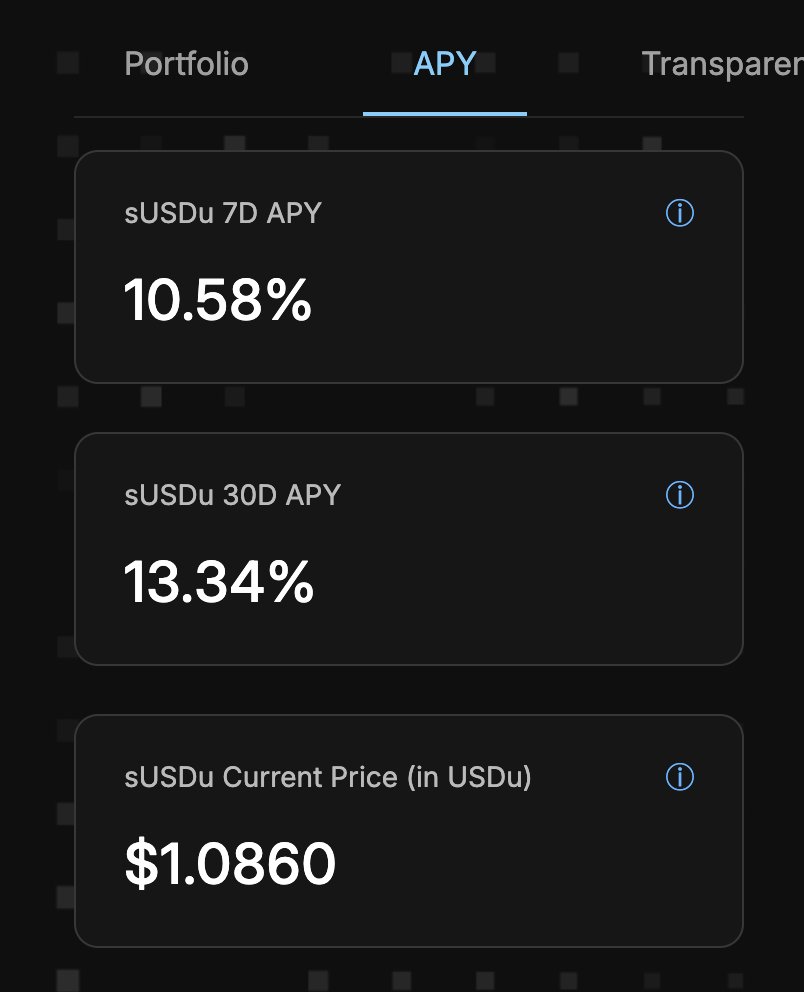

💰Step 1: Dollar yield as the base, using a market‑neutral strategy to generate ongoing income (see Fig. 2 below).

All yield protocols boil down to one question: where does the profit come from?

Unitas's foundation is USDu (a dollar asset) and sUSDu (the yield‑bearing version). Regular stablecoins only focus on pegging, while Unitas's logic is to let the professionals handle the professional work: you give me your money, I make more money, and the profit is delivered to sUSDu.

Initially, it employed a delta‑neutral strategy, deriving returns mainly from arbitraging perpetual contract funding rates in Crypto. For example, buying JLP to earn trading fees while shorting to hedge price risk. Regardless of price movement, it harvests fees and funding, funneling the profit into sUSDu. The longer you hold sUSDu, the higher the underlying USDu value becomes.

But here's the problem:

Crypto funding rates are cyclical. In a bull market, everyone goes long and rates skyrocket; in a bear market, leveraged participants dwindle, rates can even turn negative, causing a cliff‑drop in returns.

A single crypto‑asset pool has weak cyclical resilience. So it moved to step two.

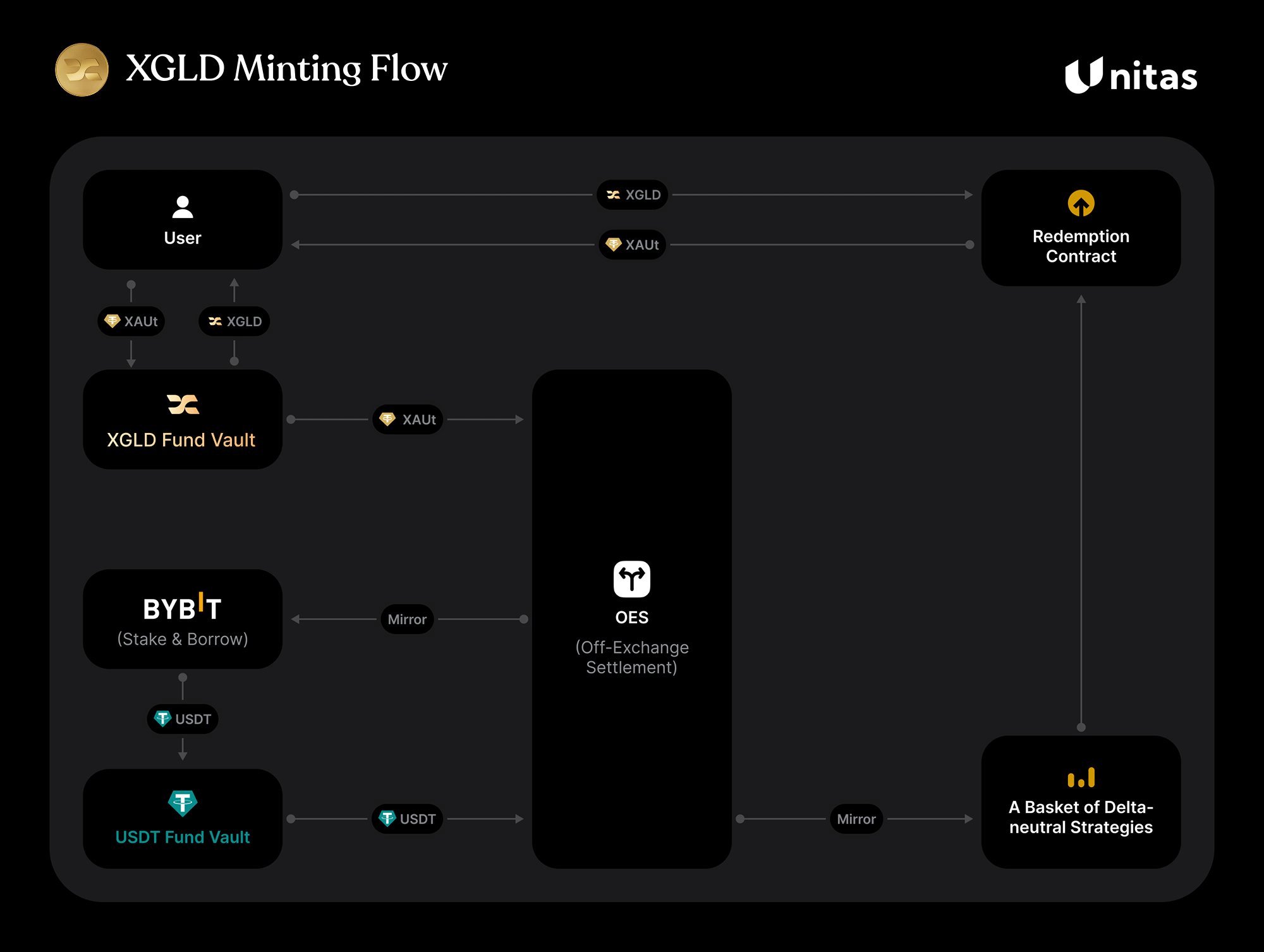

🪙Step 2: Cross‑border into gold with #XGLD, turning wealthy assets into "live" ones (see Fig. 3 below).

To avoid being hung on a single crypto funding tree, Unitas launched XGLD.

Gold is the most universally accepted safe‑haven asset, but it has a fatal flaw: it yields nothing. If you stash a ton of gold, ten years later it's still a ton, no growth.

What does Unitas do? It built a delta‑neutral yield gold product on top of XAUT.

Simply put, it smooths gold price volatility via hedging, eliminating the risk of a gold price crash, while capturing arbitrage returns from on‑chain gold derivatives.

This step shines in two ways:

• Broadening asset classes: moving from USD to gold directly opens the appetite of traditional capital and conservative institutions.

• Smoothing cycles: gold market dynamics differ completely from crypto; when crypto is flat, gold yield products can still supply steady external returns.

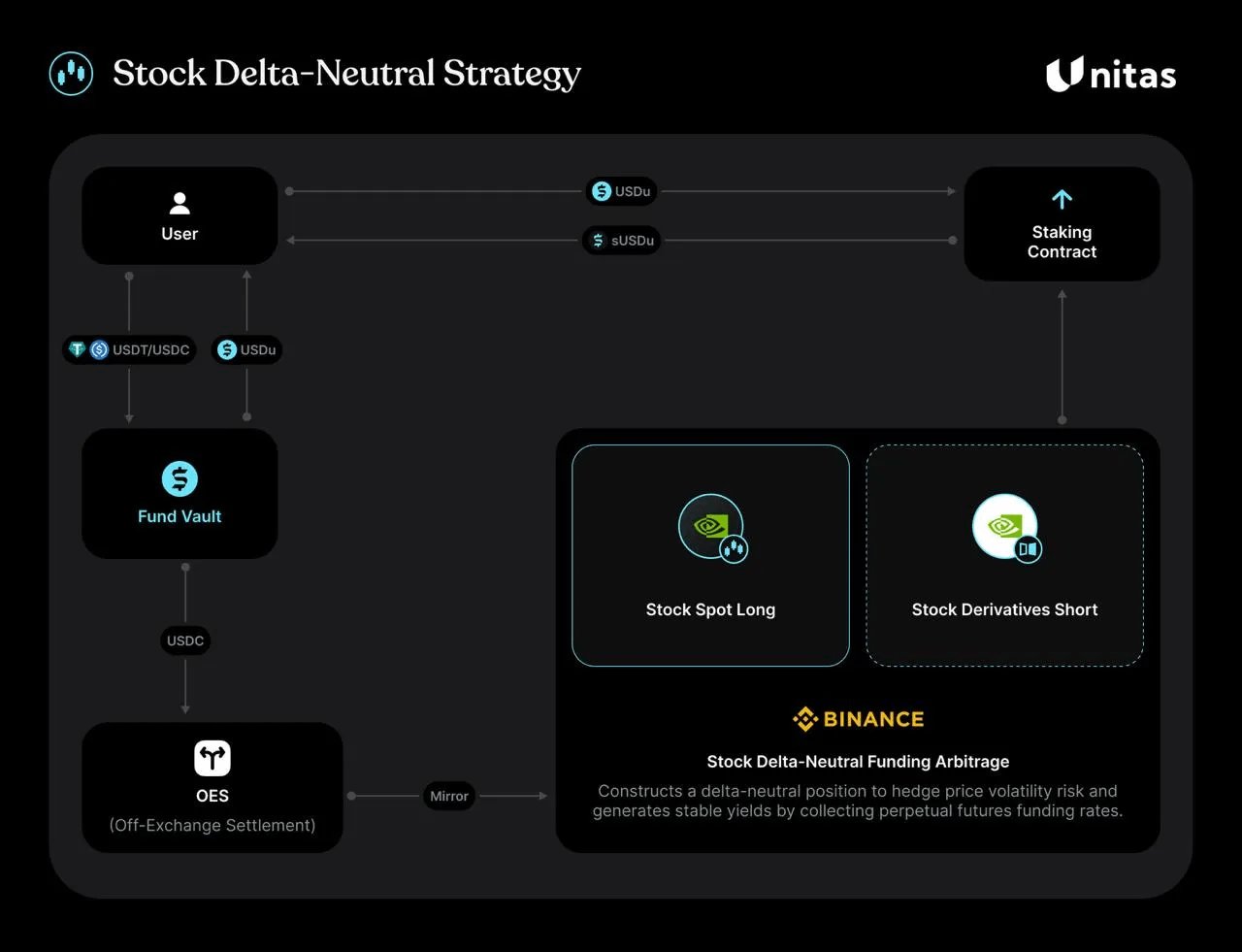

📈Step 3: The latest flagship – Equity Basis Trade – harvesting fees from US equities (see Fig. 4 below).

This is Unitas's newly announced flagship strategy, and in my view, the move that fully differentiates it from ordinary stablecoin protocols, such as #Ethena.

Since perpetual contracts in crypto have funding rates, tokenized US‑equity perpetuals have them too. Many traders go long or short US stocks on‑chain, creating arbitrage opportunities.

Unitas's new strategy:

1. Hold the spot of a particular US‑stock asset.

2. On an exchange (e.g., Binance's US‑stock spot + futures), simultaneously short the corresponding US‑stock perpetual contract.

3. The spot and short position perfectly hedge each other; US‑stock price moves are irrelevant, and the protocol simply captures the perpetual funding fees.

The brilliance of this strategy lies in the sheer size of the US‑stock market, allowing the strategy to absorb more capital. Moreover, the supply‑demand rhythm of US‑stock perpetuals is completely out of phase with Crypto. When the crypto market dips, leverage retreats, and funding turns negative, US‑stock trading can be booming, as seen in the recent AI‑hardware rally.

By tapping US‑stock funding, sUSDu’s underlying yield pool achieves genuine multi‑asset, multi‑strategy, cross‑market diversification.

Even more impressive is risk control: the team is highly restrained, initially allocating only $3‑5 million to the US‑stock strategy. It serves purely as a “validation position” to test hedging slippage, off‑hours mismatches, and other risks. Scale will be increased only after real‑world data validates the model.

Such a non‑aggressive, risk‑first approach is rare in crypto, very institutional, and deserves a big thumbs‑up 👍.

🎯Ecosystem play: why can it scale on BNB Chain?

A good strategy isn’t enough; you need a big table to play at. Unitas has recently released external signals that are overwhelming, almost like everyone is chanting its name:

• BNB Chain officially backs it. BNB Chain has over 700 million+ unique addresses and massive stablecoin TVL, low fees, fast block times—naturally suited for high‑frequency hedging strategies.

• Official recommendation from Tether’s USDT0; a dedicated yield program for Binance Wallet is en route, which is a top‑traffic gateway—once live, massive TVL will flood in.

• Has struck a strategic partnership with Hong Kong‑listed company https://t.co/uxOtDCLusE. Many talk about RWA, but they have actually opened compliant channels to listed companies and institutional capital.

I think this is no longer a single piece of good news, but a convergence of ecosystem resources, liquidity gateways, and institutional capital toward Unitas.

Finally, about $UP’s market. TVL is currently $58 million, with seven‑day average volume and price hitting all‑time highs together. When BTC is under pressure, the market still dares to price $UP, indicating not speculation but a vote for its fundamentals.

In this crypto slump, Unitas’s product logic advances a step forward periodically, with each step having tangible implementation—from dollar yield → gold RWA yield → US‑stock perpetual fee yield. This rhythm is scarce in the current market.

My personal view: the most worth‑watching aspect of Unitas isn’t today’s price, but whether it can scale this cross‑asset yield framework sufficiently.

From Crypto to gold to US equities, if this path succeeds and reaches the default $1 billion fee‑switch threshold, the yield‑asset layer on BNB Chain will essentially be dominated by it.

Once achieved, $UP’s valuation logic shifts from a stablecoin project to a on‑chain asset‑management protocol.

Feel the ceiling gap yourself. 🧐 So I will keep a long‑term watch on this project!