Comprar cripto

tarjeta

Comercio P2P

Compra USDT en un marketplace

Tarjeta de crédito/débito

Compre criptomonedas con Visa o MasterCard

Pago vía prestadores

Compre criptomonedas a través de MoonPay, Simplex y más

Tarjeta BitMart

Impulsando su experiencia con las criptomonedas

Tarjeta prepago de criptomonedas

Obtenga una Mastercard lista para usar al instante

Comerciar

USDⓈ-M

Utilizando USDⓈ como colateral

COIN-M

Utilizando la propia moneda como colateral

TradFi

Trading integral para metales, acciones y forex

Operativa de demostración

Aprenda a operar con riesgo cero

Resumen de futuros

Plataforma única para todo lo relacionado con futuros

Rey de Futuros

Pool de premios de 478 000 USDT

Crecer

Resumen de Earn

Activos inactivos, gane con facilidad

Ahorros

Gane intereses conservando su portafolio.

Staking

Staking sencillo, cuantiosas retribuciones.

Gestión de patrimonio

Aumente su riqueza con un equipo de activos top

RWA

Mantenga BMRUSD, disfrute del rendimiento

Exclusivo VIP

Gane de forma estable para usuarios VIP

Rewards

Centro de recompensas

Descubra recompensas exclusivas por valor de hasta 14 000 USDT

LaunchPrime

Una plataforma para lanzar tokens y NFT

Programa de afiliados

Únase para ganar cuantiosas comisiones

Powerdrop

¡La solución AirDrop de próxima generación ya está AQUÍ!

Centro de eventos

El centro unificado para todas las operaciones de trading

Sorteo diario de futuros

100 % de probabilidades de ganar con operaciones diarias

Sorteo diario de Spot

Gane 8888 USDT en grandes premios

Recarga móvil

Recargue móviles de forma fácil, online y segura

Send

Send money globally, fast and secure

BitMart Mall

Viva de las criptomonedas

Starter.xyz (BUIDL)

--

0%

24H

Starter.xyz BUIDL Historial de precios USD

Siga el precio de Starter.xyz para hoy, 7 días, 30 días y 90 días

Periodo

Cambiar

Cambio (%)

Hoy

--

--

7días

--

--

30días

--

--

90días

$ 0.00034

-83.33%

Sea propietario de BUIDL ahora

Compra y vende BUIDL fácil y seguro en BitMart.

Starter.xyz Información de mercado

$ 0.000069 Autonomía de 24 horas $ 0.0099

Máximo histórico

$ 0.0099

El mínimo histórico

$ 0.000069

Cambio en 24 h

Volumen en 24 h

0

Suministros en circulación

0.00

BUIDL

Market Cap

0

Suministro máximo

--

Capitalización de mercado totalmente diluida

0

Trade BUIDL

Ganar

Pon a trabajar tus criptomonedas inactivas y obtén ingresos pasivos a través de ahorros, staking y más.

Starter.xyz X Insight

Stacy Muur

OnChain_Analyst

Tokenomics_Expert

B

77.7K @stacy_muur

77.7K @stacy_muur Alcista

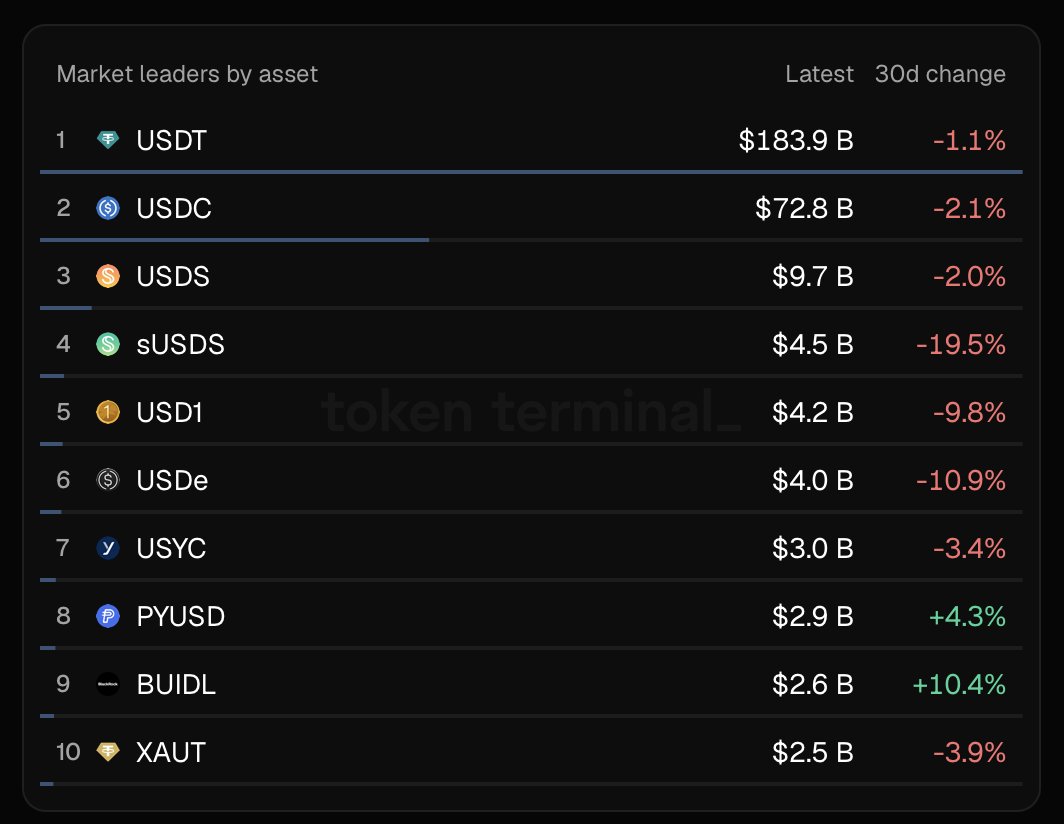

The author believes BUIDL will easily surpass USYC by the end of the year, with the image showing a monthly gain of 10.4% for BUIDL.

Stacy Muur

OnChain_Analyst

Tokenomics_Expert

B

77.7K @stacy_muur I think that $BUIDL can easily flip $USYC on this list by the end of the year https://t.co/a8cdk3XlFX

73

73

18

18

5.0K

5.0K

2026-07-25 20:27

Tendencia de BUIDL tras el lanzamiento

Alcista

The author believes BUIDL will easily surpass USYC by the end of the year, with the image showing a monthly gain of 10.4% for BUIDL.

Stacy Muur

OnChain_Analyst

Tokenomics_Expert

B

77.7K @stacy_muur Alcista

The author believes BUIDL will easily surpass USYC by the end of the year, with the image showing a monthly gain of 10.4% for BUIDL.

I think that $BUIDL can easily flip $USYC on this list by the end of the year https://t.co/a8cdk3XlFX

73

18

5.0K

2026-07-25 08:17

Tendencia de BUIDL tras el lanzamiento

Alcista

The author believes BUIDL will easily surpass USYC by the end of the year, with the image showing a monthly gain of 10.4% for BUIDL.

MSB Intel

Media

Influencer

B

39.6K @MSBIntel Neutral

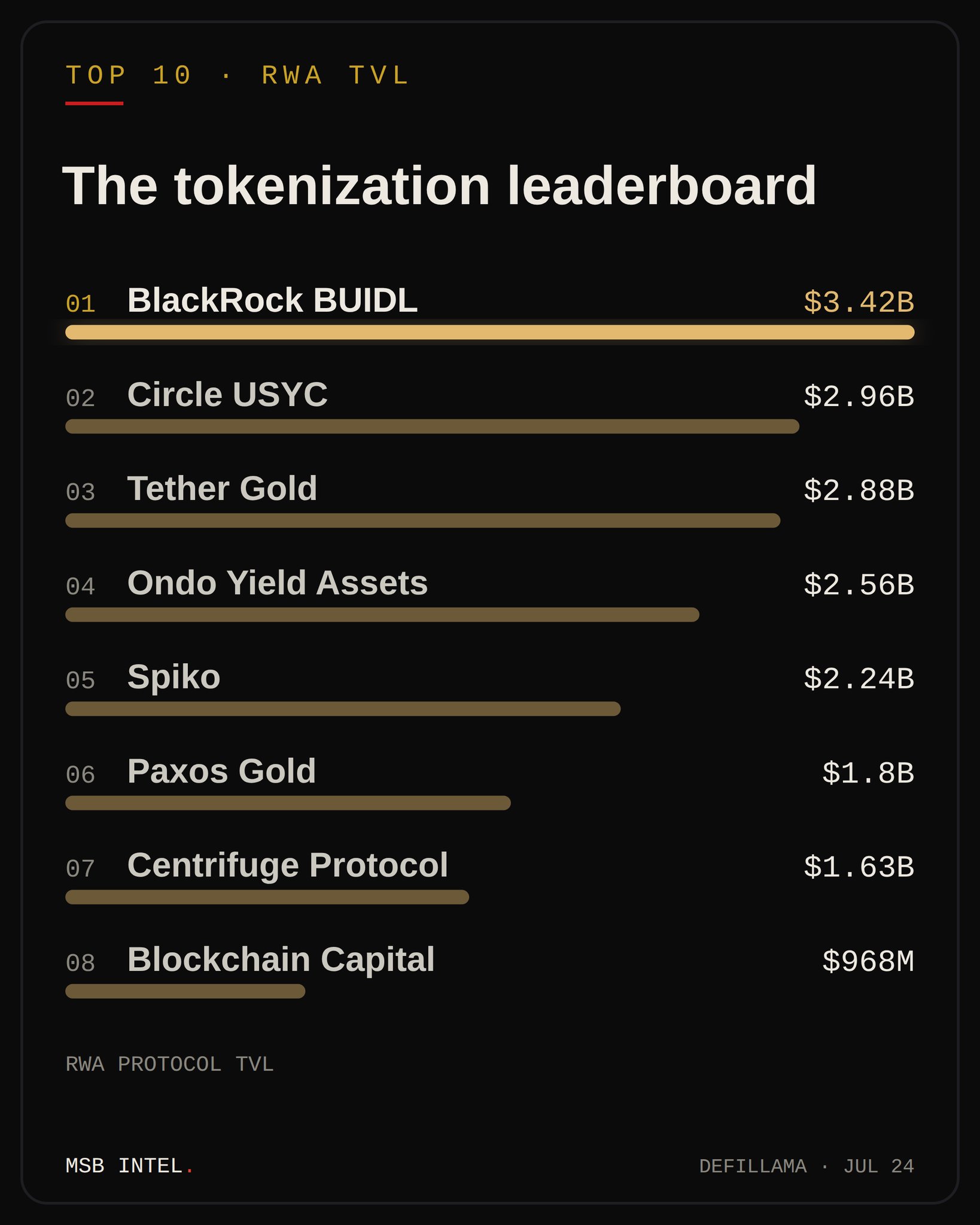

BlackRock BUIDL leads the RWA tokenization ranking with $3.42B TVL.

INSIGHT: BlackRock BUIDL leads RWA TVL at $3.42B.

Circle USYC follows at $2.96B. Tether Gold holds third at $2.88B. https://t.co/m8f5ZfKoWX

10

1

1.5K

10

1

1.5K

2026-07-24 03:27

Tendencia de BUIDL tras el lanzamiento

Neutral

BlackRock BUIDL leads the RWA tokenization ranking with $3.42B TVL.

Sobre Starter.xyz

Starter.xyz (BUIDL) is a cryptocurrency launched in 2024and operates on the Base platform. Starter.xyz has a current supply of 213,982,042.545 with 0 in circulation. The last known price of Starter.xyz is 0.00006867 USD and is up 0.00 over the last 24 hours. More information can be found at https://starter.xyz.

Leer más

Enlaces oficiales

Explorador de blockchain