I am so bullish on $SKY right now.

This inverted head and shoulder gave us a reason.

$0.70 is the first target.

$0.75 is the second one.

5th consecutive positive quarter. The money is flowing in. https://t.co/aL06QIeBLn

5.2K @oct_trades

5.2K @oct_trades I am so bullish on $SKY right now.

This inverted head and shoulder gave us a reason.

$0.70 is the first target.

$0.75 is the second one.

5th consecutive positive quarter. The money is flowing in. https://t.co/aL06QIeBLn

5.4K @SkyMoney

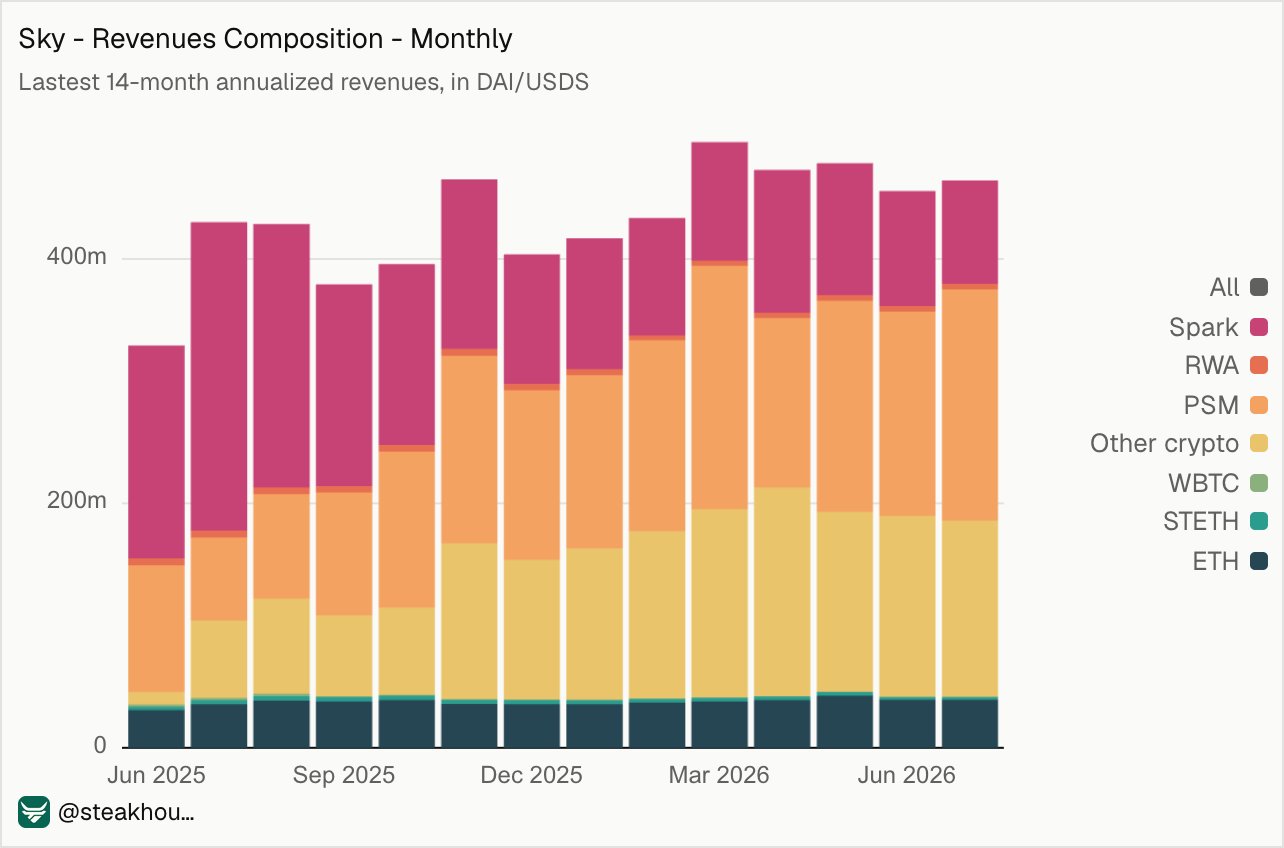

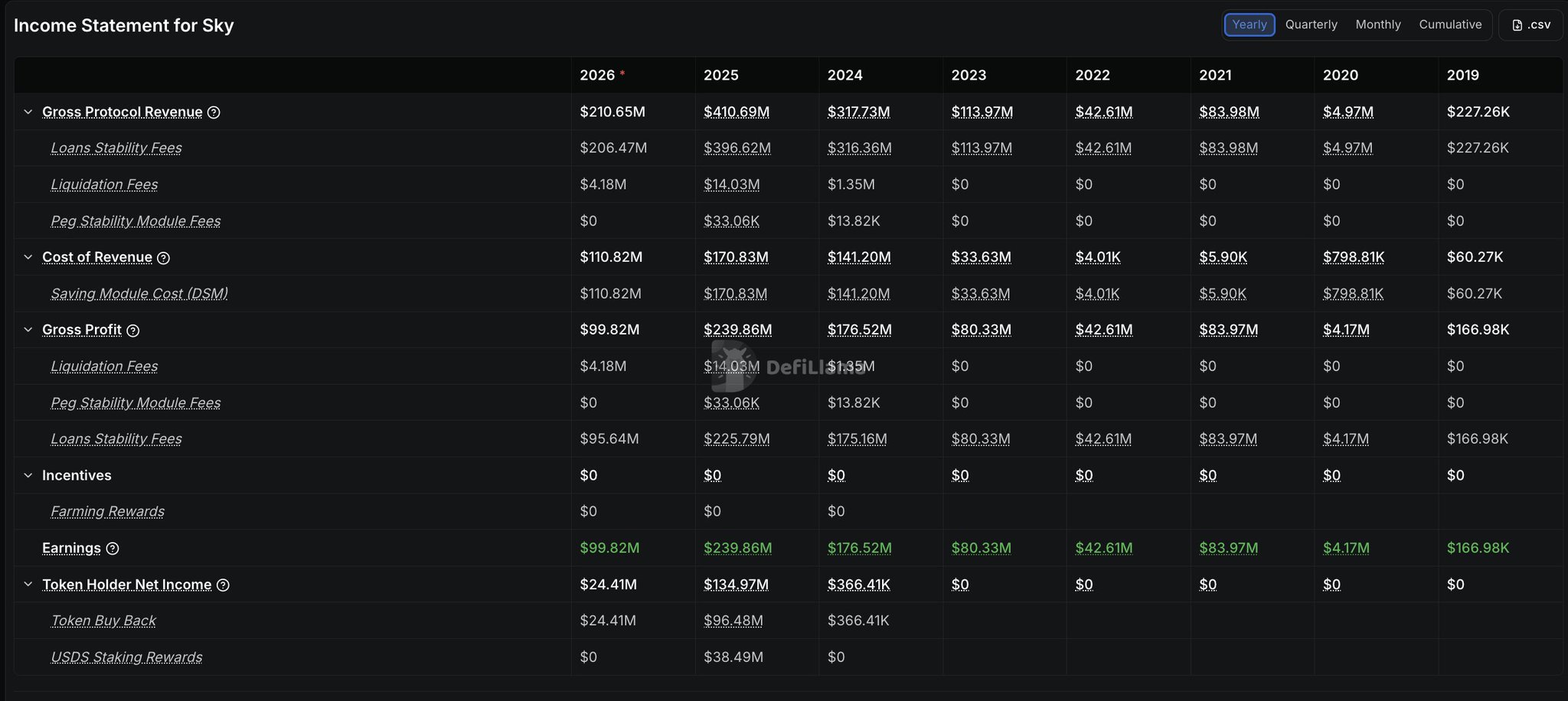

5.4K @SkyMoney Sky Protocol registered its fifth consecutive positive quarter in Q2 2026, generating $107.35M Gross Protocol Revenue & $33.29M Net Protocol Surplus.

In Q2 2026, cumulative value distributed through the Sky Savings Rate surpassed $250M since inception.

Read the full report ↓

8

8

2

2

594

594

9.4K @YashasEdu

9.4K @YashasEdu In my opinion @SkyEcosystem is one of the highest conviction plays in established DeFi as it combines...

1. bluechip CDP leader

2. genuine rev +ve business with strong margins

3. diversified real yields

4. buyback/burn/staking value accrual

Right now ethereum:0x56072c95faa701256059aa122697b133aded9279 is mispriced cheap relative to peers and relative to its own resilience through the current market drawdown.

h/t to @Dune @DefiLlama for the data

25

10

1.7K

25

10

1.7K

29.3K @beracap

29.3K @beracap I think $Sky is being slept on

6

0

2.1K