$NVDA: Kyber Delays?

Kyber is the rack architecture for VR300, not the current release of VR200 which will use the Oberon racks.

I appreciate @Aaronwei3n for sticking to his guns on Kyber delay rumors. Nvidia will not announce until it has to but Aaron is boots on the ground and seeing the signs now already due to orthogonal midplane difficulty.

Note there is nothing wrong with state of the art GPU system level delays as that is normal with such a complex system. Aaron himself states single digit percentage impacts to revenue for $NVDA. Suppliers may get impacted more majorly.

Interest to $IREN investors is that we will need 600kW rack density and 800V DC power distribution system. @FransBakker9812 for viz.

Not that $INV is not the provider of two stage cooling for Kyber but rather Asia Vital Components (3017 TT) and Cooler Master. @MarkosAAIG @MB_Hogan for viz.

Купить криптовалюту

карта

P2P Трейдинг

Купить USDT через маркетплейс

Кредитная/дебетовая карта

Покупайте криптовалюту с помощью карт Visa или Mastercard

Оплата третьей стороной

Buy Crypto via MoonPay, Simplex and More

Карта BitMart

Расширение ваших криптовозможностей

Предоплаченная криптовалютная карта

Мгновенно получите карту Mastercard, доступную для использования

USDⓈ-M

Использовать USDⓈ в качестве обеспечения

COIN-M

Использовать монету в качестве обеспечения

TradFi

Единый центр торговли металлами, акциями и иностранной валютой

Демо-торговля

Узнайте, как торговать с нулевым риском

Фьючерсная торговля

Универсальная платформа для фьючерсной торговли

Futures King

478,000 USDT Prize Pool

Grow

Обзор программы Earn

Без труда зарабатывайте на незадействованных активах

Сбережения

Зарабатывайте проценты на холдинге

Стейкинг

Простой стейкинг и хорошие вознаграждения

Управление капиталом

Grow Wealth with a Top-Tier Asset Team

RWA

Удерживайте BMRUSD и получайте доход

VIP-эксклюзив

Стабильный заработок для VIP-пользователей

Rewards

Центр вознаграждений

Discover Exclusive Rewards Worth Up to 14,000 USDT

LaunchPrime

Платформа для запуска NFT и токенов

Партнерская программа

Присоединяйтесь к программе, чтобы зарабатывать высокие комиссионные

Powerdrop

Запущено решение для Аирдропов нового поколения!

Центр событий

The One-Stop Hub For All Business Operations

Futures Daily Draw

100% Chance To Win With Daily Trades

Spot Daily Draw

Win 8,888 USDT In Grand Prizes

Участвуйте в стейкинге для голосования

Заработайте эйрдропы, проголосовав

Учреждение

Профессиональные и эксклюзивные сервисы

VIP

Разблокируйте Эксклюзивные Награды

Академия

Быстро изучите трейдинг и блокчейн

BitMart Internship

Start your Crypto Career Here

Bitmart Путешествия

One-Stop Global Travel Services

Mobile Top-Up

Top up mobiles easily, online, secure

Send

Send money globally, fast and secure

BitMart Mall

Live on crypto

NVIDIA (Derivatives) (NVDA)

$ 198.87 (NVDA/USD)

-0.04%

24H

NVIDIA (Derivatives) NVDA Price History USD

Track the price of NVIDIA (Derivatives) for today, 7 days, 30 days and 90 days

Период

Изменить

Изменение (%)

Сегодня

$ 0.079

-0.04%

7дней

$ 7.46

-3.61%

30дней

$ 2.11

1.07%

90дней

$ 8.06

-3.89%

Own NVDA Now

Buy and sell NVDA easily and securely on BitMart.

NVIDIA (Derivatives) Информация о рынке

$ 198.56 24 часа $ 199.82

Рекордный максимум

$ 240.42

Рекордный минимум

$ 162.98

Изменение за 24 часа

-0.04%

Объем за 24 часа

$ 59,936.45

Количество токенов в обороте

0.00

NVDA

Рыночная капитализация

$ 0

Максимальное предложение

--

Рыночная капитализация при полной эмиссии

$ 0

Торговать NVDA

Заработать

Даже незадействованная криптовалюта может приносить пассивный доход! Пользуйтесь сбережениями, услугами стейкинга и другими преимуществами.

NVIDIA (Derivatives) Инсайт из X

Jim Liu D

30.2K @jiahanjimliu

30.2K @jiahanjimliu Нейтрально

NVDA Kyber delay, revenue impacted by single‑digit figures

Jim Liu D

30.2K @jiahanjimliu Nvidia has denied but I believe Aaron and @SemiAnalysis_ on this one. https://t.co/G8pUMYSmL6

28

28

5

5

11.6K

11.6K

2026-07-22 05:27

Тренд NVDA после выпуска

Нейтрально

NVDA Kyber delay, revenue impacted by single‑digit figures

materkel.eth 🦇🔊

FA_Analyst

Influencer

A

5.8K @materkel Чрезвычайно бычий

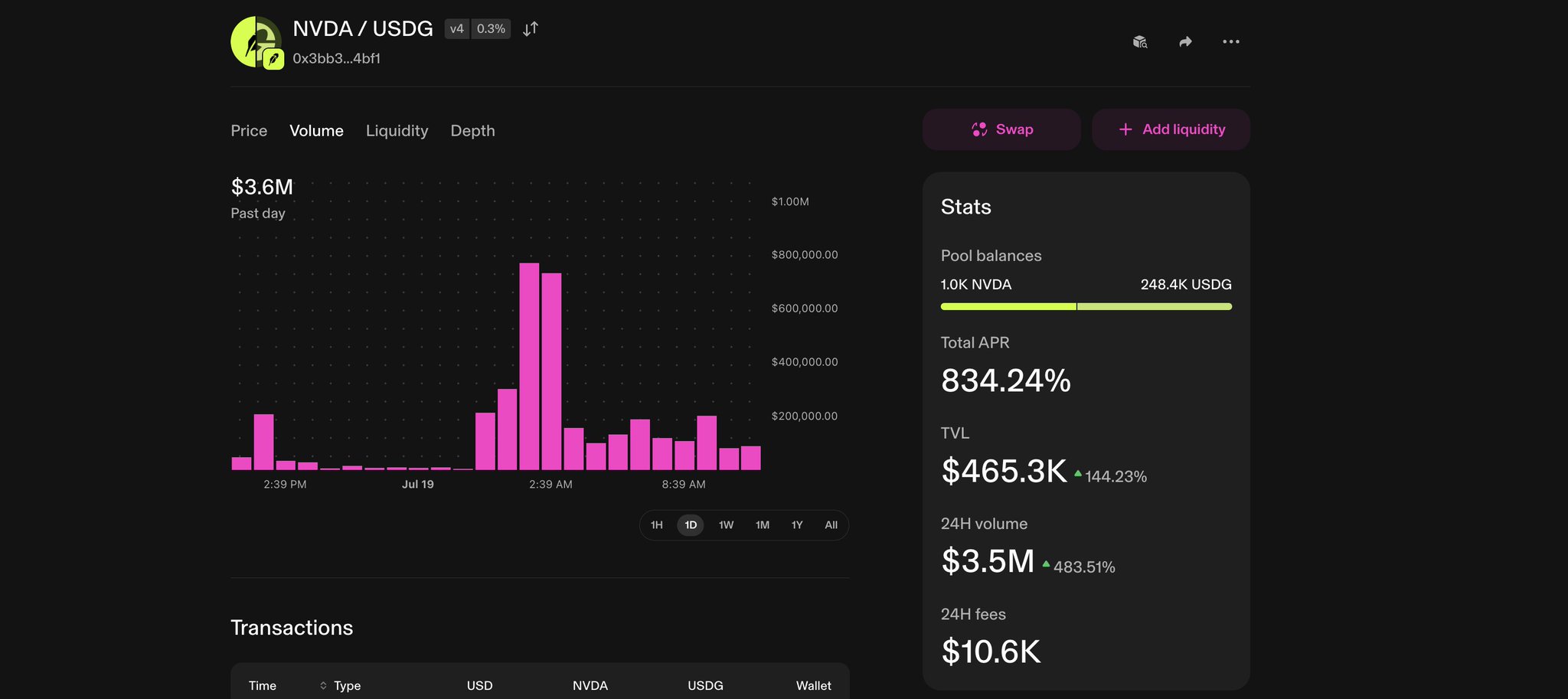

NVDA/USDG Uniswap V4 pool becomes the largest RWA pool on the Robinhood chain, with a huge increase in trading volume and TVL.

Hayden Adams 🦄 D

1.0M @haydenzadams Update: the numbers are going up quickly

the largest rwa pool on Robinhood chain is now a NVIDA/USDG Uniswap v4 pool with $3.5m in daily trading volume https://t.co/63nreUxh0T

819

132

202.4K

819

132

202.4K

2026-07-20 19:47

Тренд NVDA после выпуска

Чрезвычайно бычий

NVDA/USDG Uniswap V4 pool becomes the largest RWA pool on the Robinhood chain, with a huge increase in trading volume and TVL.

Stablecoin Sean

FA_Analyst

OnChain_Analyst

B

24.5K @seanlippel Чрезвычайно бычий

The NVDA/USDG Uniswap v4 pool has become the largest RWA pool on the Robinhood chain, with TVL and trading volume significantly increasing, and APR exceeding 800%.

Hayden Adams 🦄 D

1.0M @haydenzadams Update: the numbers are going up quickly

the largest rwa pool on Robinhood chain is now a NVIDA/USDG Uniswap v4 pool with $3.5m in daily trading volume https://t.co/63nreUxh0T

819

132

202.4K

2026-07-20 18:57

Тренд NVDA после выпуска

Чрезвычайно бычий

The NVDA/USDG Uniswap v4 pool has become the largest RWA pool on the Robinhood chain, with TVL and trading volume significantly increasing, and APR exceeding 800%.

Прогнозирование цен

When is a good time to buy NVDA? Should I buy or sell NVDA now?

When deciding whether it’s a good time to buy or sell NVIDIA (Derivatives) (NVDA), it’s important to first align with your own trading strategy and risk profile.Long-term investors and short-term traders often interpret market conditions differently, so your decision should reflect your personal approach. According to the latest NVDA 4-hour technical analysis, the current trading signal is Hold. According to the latest NVDA 1-day technical analysis, the current signal is Продать.

Прогноз Beacon

Probabilistic Price Forecast (Next 24 Hours)Отказ от ответственности за прогноз Beacon

The data results displayed on this page are analyzed based on actual trading data (OHLCV) of the selected trading pair along with corresponding technical indicators.

This prediction is an experimental technical product and is provided for reference purposes only. It does not constitute investment advice. Unexpected real-world events may significantly impact market behavior. Traders should make decisions with caution.

This prediction is an experimental technical product and is provided for reference purposes only. It does not constitute investment advice. Unexpected real-world events may significantly impact market behavior. Traders should make decisions with caution.

О нас NVIDIA (Derivatives)

NVIDIA (Derivatives) (NVDA) is a cryptocurrency . NVIDIA (Derivatives) has a current supply of 0. The last known price of NVIDIA (Derivatives) is 208.68157837 USD and is up 0.29 over the last 24 hours. It is currently trading on 89 active market(s) with $0.00 traded over the last 24 hours.

Читать далее