LISTA Swing/Spot play.

Entry zone : 0.046 - 0.049

TPs: 0.053 / 0.0541 / 0.057 / 0.064 / 0.071 / 0.079 / 0.088 / 0.094

Sl 0.044

Купити криптовалюту

Картка

P2P-торгівля

Купуйте USDT через маркетплейс

Кредитна/дебетова картка

Купуйте криптовалюту за допомогою Visa або MasterCard

Платіж третьої сторони

Купуйте криптовалюту через MoonPay, Simplex та інші сервіси

Картка BitMart

Розширення можливостей вашого криптожиття

Передплачена криптовалютна картка

Миттєво отримайте картку Mastercard для витрат

Торгувати

USDⓈ-M

Використання USDⓈ в якості застави

COIN-M

Використання самої COIN в якості застави

TradFi

Єдине місце для торгівлі металами, акціями та іноземною валютою

Демоторгівля

Дізнайтеся, як торгувати без ризику

Огляд ф'ючерсів

Універсальна платформа для всього, що стосується ф'ючерсів

Futures King

Призовий фонд 478 000 USDT

Примножити

Детальніше про Earn

Заробляйте на невикористаних активах із легкістю

Заощадження

Заробляйте на холдингу.

Стейкінг

Легка ставка, висока винагорода.

Управління капіталом

Примножуйте свій капітал із допомогою провідної команди в галузі управління активами

RWA

Утримуйте BMRUSD — отримуйте дохід

VIP-ексклюзив

Стабільно заробляйте для VIP-користувачів

AI Hub

Rewards

Щоденний розіграш ф’ючерсів

100% шанс на перемогу на щоденних угодах

Щоденний спотовий розіграш

Виграйте головний приз — до 8 888 USDT

Ставка для голосування

Заробіть айрдропи, проголосувавши

Установа

Професійні та ексклюзивні послуги

VIP

Розблокуйте ексклюзивні винагороди

Академія

Швидко дізнайтеся про трейдинг та блокчейн

BitMart Internship

Start your Crypto Career Here

Bitmart подорожі

Універсальні глобальні туристичні послуги

Поповнення мобільного

Швидке і безпечне поповнення мобільного онлайн

Send

Send money globally, fast and secure

BitMart Mall

Заробляйте криптовалюту

Lista DAO Дані про ціни в реальному часі

Поточна ціна Lista DAO становить $ 0.049 (LISTA/USD). З ринковою капіталізацією $ 21.64M USD. Обсяг торгів за 24 години: $ 546.41K USD, Зміна ціни за 24 години: +0.41%, І циркулююча пропозиція: 438.42M LISTA.

Lista DAO LISTA Історія зміни цін USD

Відстежуйте зміну ціни Lista DAO за сьогодні та за 7, 30 і 90 днів

Період

Змінити

Зміна (%)

Сьогодні

$ 0.00019

0.41%

7днів

$ 0.0029

-5.73%

30днів

$ 0.0022

-4.45%

90днів

$ 0.039

-44.43%

Стати власником LISTA зараз

Купуйте та продавайте LISTA легко та безпечно на BitMart.

Lista DAO Інформація про ринок

$ 0.048 24-годинний діапазон $ 0.049

Найвищий показник за весь час

$ 0.85

Найнижчий показник за весь час

$ 0.044

24-годинна зміна

0.41%

24г Vol

$ 546,405.54

Циркуляційний запас

254.61M

LISTA

Ринкова капіталізація

$ 12.57M

Максимальна пропозиція

1.00B

LISTA

Повністю розбавлена ринкова капіталізація

$ 49.37M

Торгувати LISTA

Заробити

Залучайте неактивну криптовалюту до роботи та легко отримуйте пасивний дохід через заощадження, стейкінг та інші послуги.

Lista DAO X Інсайт

CryptoDoc (Gem Hunter💎)

TA_Analyst

Trader

C

79.8K @cryptodoc_

79.8K @cryptodoc_ Бичачий

Buy LISTA in the 0.046‑0.049 range, target price 0.088 bullish

12

12

4

4

7.5K

7.5K

2026-07-03 07:57

Тенденція LISTA після випуску

Бичачий

Buy LISTA in the 0.046‑0.049 range, target price 0.088 bullish

토큰포스트 - TokenPost Korea

Media

Influencer

D

5.7K @tokenpostkr Бичачий

ListaDAO clarifies that the third‑party contract vulnerability does not affect its own core contracts.

ListaDAO "The reported vulnerable contract was created by a third party... no damage to our contract"

https://t.co/mmhmCijtZr https://t.co/anbyjftfT7

0

0

23

0

0

23

2026-04-17 06:12

Тенденція LISTA після випуску

Бичачий

ListaDAO clarifies that the third‑party contract vulnerability does not affect its own core contracts.

机灵的杰尼君🔶BNB

Trader

Quant

C

107.4K @Meta8Mate Надзвичайно бичачий

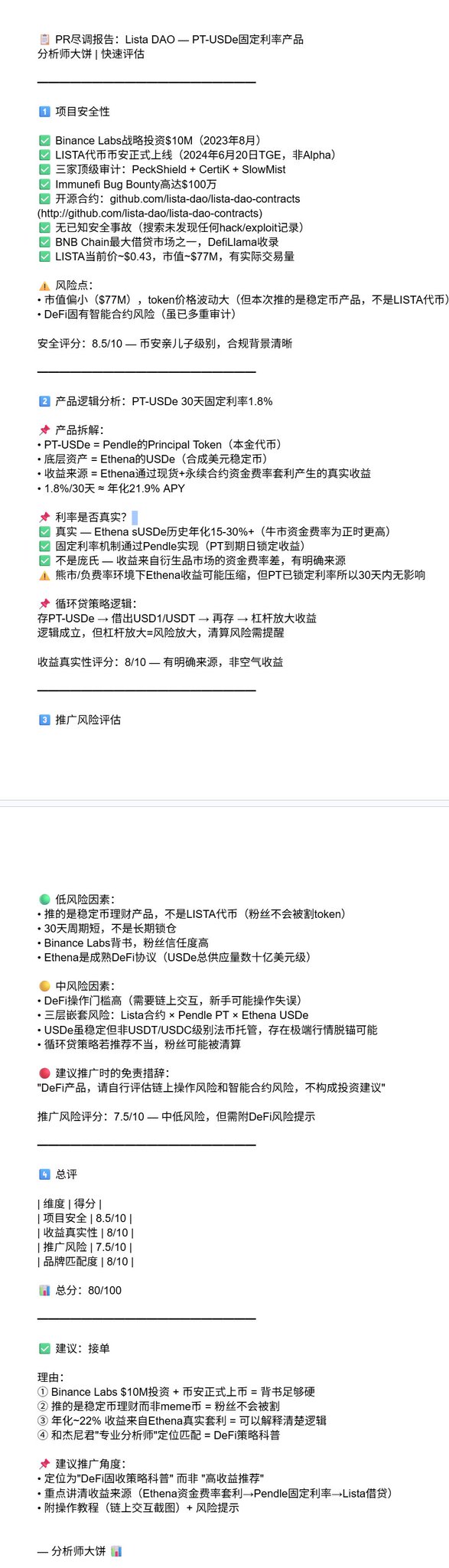

Lista DAO fixed-rate lending strategy, using PT-sUSDe to achieve near-zero-cost borrowing, with high yield potential.

Using Jeni Jun's Little Lobster team @openclaw conducted due diligence on @lista_dao, and the process was somewhat surprising.

Project safety, yield authenticity, promotional risk, brand match – all were completed in minutes, each with clear conclusions.

Suddenly realized: this setup is naturally suited for the crypto space; once AI due diligence becomes the norm, RUG projects will have nowhere to hide — it’s another form of “good money drives out bad money”.

Crypto retail investors get rug pulled not often because they don’t understand, but because of information asymmetry. AI can fill this gap, even partially, and I think it’s worthwhile.

Of course, I’m not saying AI due diligence is omnipotent; it can also be fooled, but it raises the cost of malicious behavior.

Do you think AI can reduce your chances of being rug pulled?

机灵的杰尼君🔶BNB

Trader

Quant

C

107.4K @Meta8Mate The 杰尼君OpenClaw team, after detailed research, brings the first project @lista_dao. The due diligence report will be posted in the comments later and serves as a comprehensive project investigation for reference.

***

Recently, the Lobster team conducted a DeFi project study; the product logic is rather unique and deserves a dedicated explanation.

The product is Lista DAO @lista_dao's PT-sUSDe fixed-rate lending market. The core selling point is: your collateral earns money while the borrowing cost is almost fully covered — near‑free borrowing.

Let's break down the three-layer protocol:

Layer 1: Ethena's $sUSDe

$sUSDe is Ethena's staked synthetic USD. It captures funding rates by holding spot BTC/ETH and shorting an equal amount of perpetual contracts, then adds ETH staking rewards. Historically it yielded 10‑20%+ annualized; currently about 3.5% annualized. In short, it is a stablecoin that generates its own interest.

Layer 2: Pendle's split

Pendle is the leading protocol in the DeFi fixed‑income space. It splits sUSDe into two tokens.

PT-sUSDe is the principal token, bought at a discount and redeemed 1:1 for sUSDe at maturity, similar to a zero‑coupon bond in DeFi. Current fixed annual yield is about 3.7‑3.9%, with a maturity around April 9 2026. The return is locked in advance and not affected by subsequent sUSDe rate fluctuations.

YT is the yield token that captures all variable returns; it is a high‑risk, high‑leverage product and is out of scope for this discussion.

Layer 3: New feature of Lista DAO

Lista DAO is one of the largest lending + CDP + liquidity‑staking protocols on BNB Chain. Binance Labs made a strategic investment of $10M in 2023, TVL peaked at $4.3 billion, token $LISTA launched on Binance Launchpool in June 2024, audited by PeckShield, CertiK and SlowMist, with a $1 million Immunefi bug bounty, and no security incidents to date.

The newly launched feature allows using PT-sUSDe as collateral to borrow $U or $USD1 stablecoins at a fixed annual cost of roughly 1.8%. Two markets are supported; you can choose which stablecoin to borrow as needed.

Core logic:

PT-sUSDe carries an inherent fixed annual yield of about 3.9%, while Lista’s borrowing cost is only about 1.8% annualized — fixed.

The spread is roughly 2%, meaning the earnings on the collateral each year are enough to cover the borrowing interest, with surplus left over.

In other words, the borrowed stablecoin is obtained at almost zero cost; using that capital elsewhere yields pure spread profit.

Two strategies in detail:

Strategy 1 (conservative): collateral‑then‑invest

Step 1: Deposit PT-sUSDe into Lista as collateral.

Step 2: Borrow USD1 or U at a fixed 1.8% annual rate.

Step 3: Deposit the borrowed stablecoin into Binance Savings (USD1 once had a 20% annual promotion) or other CEX savings products.

Step 4: When PT matures (around April 9), redeem sUSDe 1:1, repay the loan, and settle profits.

Advantages of this strategy: dual‑layer yield stacking, no active management needed, PT auto‑settles at maturity, clear logic, suitable for users who do not want to constantly manage positions.

Strategy 2 (advanced): fixed‑rate circular lending

Step 1: Deposit PT-sUSDe as collateral and borrow stablecoins.

Step 2: Swap the stablecoins for sUSDe, then buy more PT-sUSDe on Pendle.

Step 3: Deposit the newly bought PT back into Lista, borrow again, and repeat.

Step 4: Theoretical leverage of 3‑5×, estimated net annual return about 10%.

The core value of this strategy lies in the fixed rate: the borrowing cost of 1.8% annualized is locked, regardless of market rate changes, so your borrowing cost does not increase and you won’t be forced to liquidate due to rate swings. This is the biggest difference between fixed and variable rates — predictable cost and executable strategy.

What is USD1: USD1 is a USD‑pegged stablecoin issued by World Liberty Financial (WLFI). It launched on Binance at the end of 2025 and is currently the second‑largest borrowed asset on Lista.

⚠️ Risks must be taken seriously:

Maturity mismatch risk: PT matures around April 9; loan terms should align, otherwise exiting PT early incurs a discount loss.

Liquidation risk: Fixed rate does not mean risk‑free; a drop in PT price mid‑term can still trigger liquidation, which is often overlooked.

Three‑layer contract nesting: Lista × Pendle × Ethena; an issue in any layer affects the whole, and while Lista has triple audits, zero risk is not guaranteed.

Circular lending risk: Leverage amplifies both returns and liquidation exposure; not recommended for those without DeFi experience.

Opportunity cost: Funds are locked until PT matures and cannot be exited without loss.

***

This is the research share from 杰尼君 and the Lobster team. All data are as of the research date, do not constitute investment advice, principal loss risk exists, please assess yourself, DYOR.

@lista_dao @Ethena_Eco @pendle_fi @ethena

16

11

6.2K

16

11

6.2K

2026-03-11 02:51

Тенденція LISTA після випуску

Надзвичайно бичачий

Lista DAO fixed-rate lending strategy, using PT-sUSDe to achieve near-zero-cost borrowing, with high yield potential.

Прогноз ціни

Чи зараз слушний час для покупки LISTA? Чи варто зараз купувати або продавати LISTA?

Вирішуючи, чи вдалий зараз час для купівлі або продажу Lista DAO (LISTA), важливо спочатку узгодити свою торгову стратегію та профіль ризику.Довгострокові інвестори та короткострокові трейдери часто по-різному інтерпретують ринкові умови, тому ваше рішення має відображати ваш особистий підхід. Згідно з останнім 4-годинним технічним аналізом LISTA, поточний торговий сигнал — Утримувати. Згідно з останнім 1-денним технічним аналізом LISTA, поточний сигнал — Продати.

Прогноз Beacon

Ймовірний прогноз ціни (на найближчі 24 години)Відмова від відповідальності щодо передбачення Beacon

Результати даних, відображені на цій сторінці, аналізуються на основі фактичних торгових даних (OHLCV) обраної торгової пари разом із відповідними технічними показниками.

Цей прогноз є експериментальним технічним продуктом і надається лише для довідки. Він не є інвестиційною порадою. Несподівані події в реальному світі можуть суттєво вплинути на поведінку ринку. Трейдерам слід приймати рішення з обережністю.

Цей прогноз є експериментальним технічним продуктом і надається лише для довідки. Він не є інвестиційною порадою. Несподівані події в реальному світі можуть суттєво вплинути на поведінку ринку. Трейдерам слід приймати рішення з обережністю.

Про Lista DAO

Lista DAO (LISTA) is a cryptocurrency launched in 2022and operates on the BNB Smart Chain (BEP20) platform. Lista DAO has a current supply of 795,588,564.255041 with 438,422,698.7744087 in circulation. The last known price of Lista DAO is 0.05036551 USD and is down -1.19 over the last 24 hours. It is currently trading on 175 active market(s) with $3,448,717.58 traded over the last 24 hours. More information can be found at https://lista.org/.

Читати більше

Офіційні посилання

Соціальні мережі

Дослідник ланцюга

Дізнатись більше

Огляд BM

Новий лістинг

HALON Halliburton

-- 0.00%

WMBON Williams Companies

-- 0.00%

STMON STMicroelectronics

-- 0.00%

EQTON EQT Corporation

-- 0.00%

APHON Amphenol

-- 0.00%

TIPON iShares TIPS Bond ETF

-- 0.00%

SYMON Symbotic

-- 0.00%

COPXON Global X Copper Miners ETF

-- 0.00%

SLBON SLB

-- 0.00%

LCAI Lightchain AI

-- 0.00%

Купити LISTA

Торгувати LISTA